Job Growth Misses Expectations as Hiring Cools: What June 2026 Means for Mortgage Rates and Housing

As of June 28, 2026, the labor market is sending a mixed but important signal. Job growth cooled versus expectations, but unemployment remained low, job openings stayed steady, and wage growth was still firm. For anyone tracking mortgage rates, home affordability, or housing demand, that combination matters more than any single headline.

The key takeaway is simple: the job market is cooling, not cracking. That is very different from a labor market that would push the Federal Reserve to cut rates quickly. For real estate, that distinction helps explain why mortgage rates remain elevated even as some housing activity continues to surprise on the upside.

📊 The big picture on the June 2026 jobs data

Three major labor indicators were in focus:

- Employment Situation report for June

- ADP National Employment Report for June

- JOLTS report for May, which tracks job openings and labor turnover

Taken together, they point to a labor market that is still healthy enough to keep the Fed cautious on rate cuts.

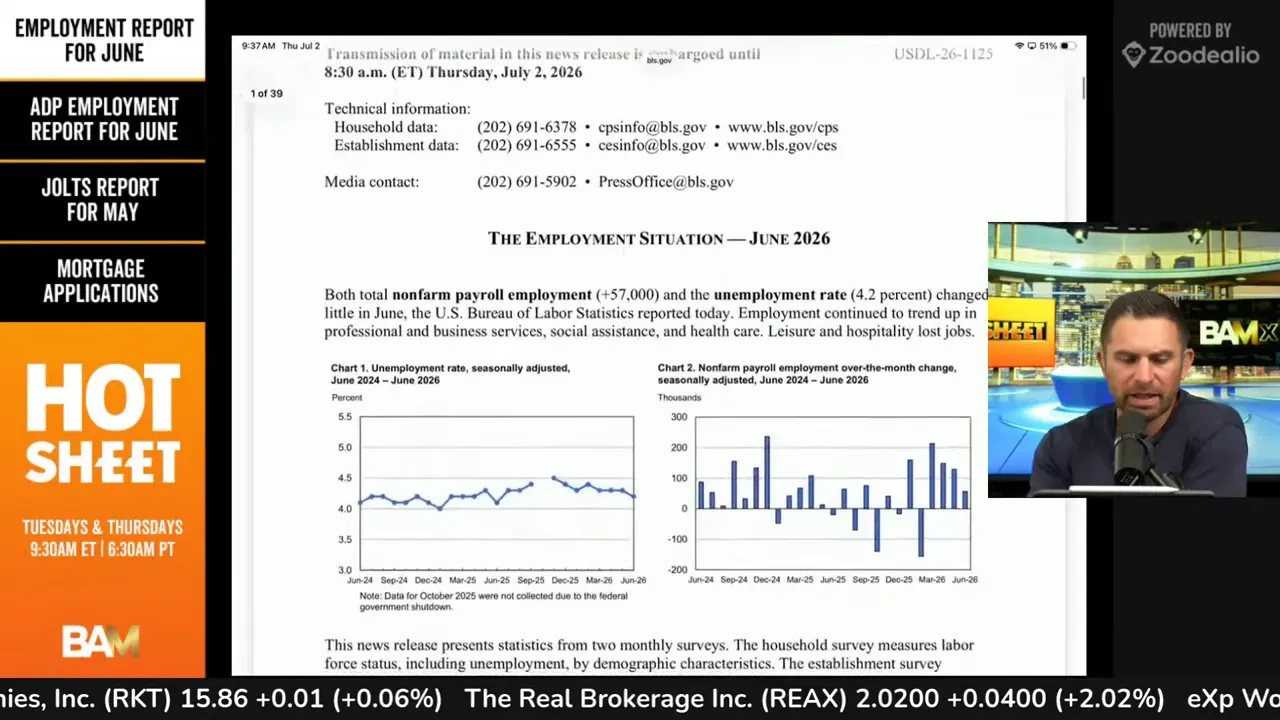

The most important headline numbers were:

- Nonfarm payrolls rose by 57,000 in June

- Unemployment held at 4.2%

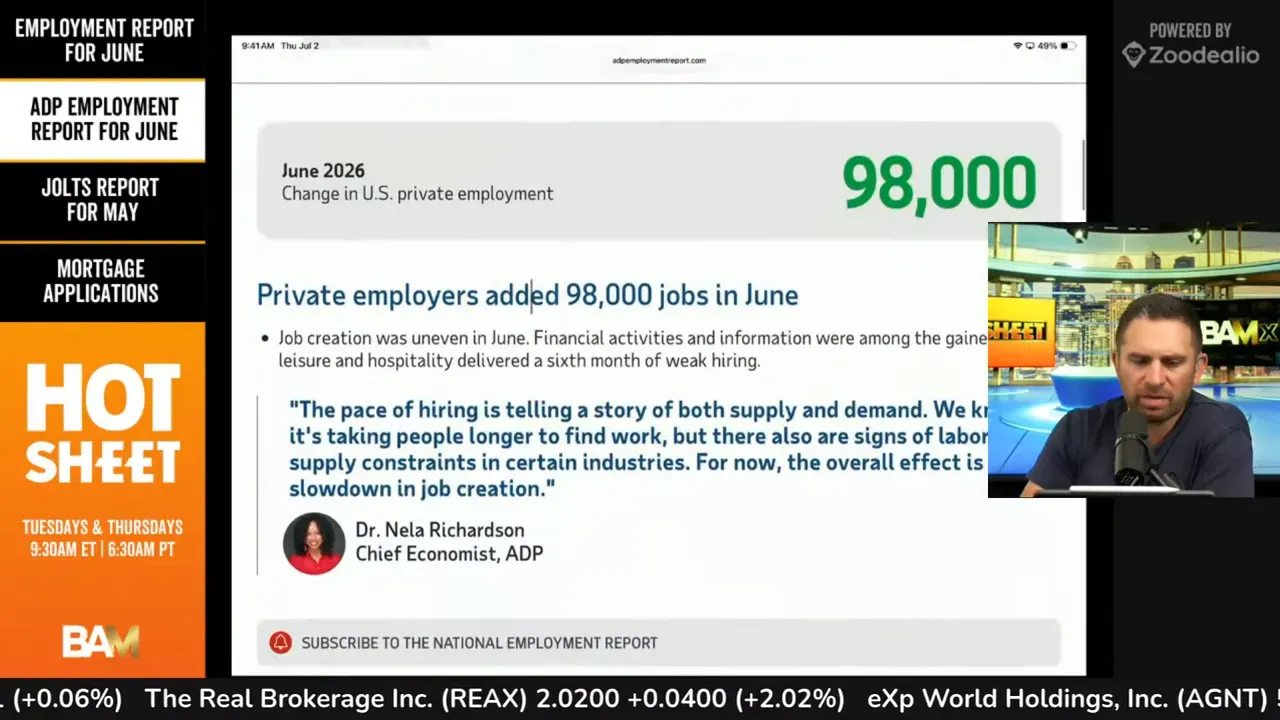

- ADP private employment increased by 98,000

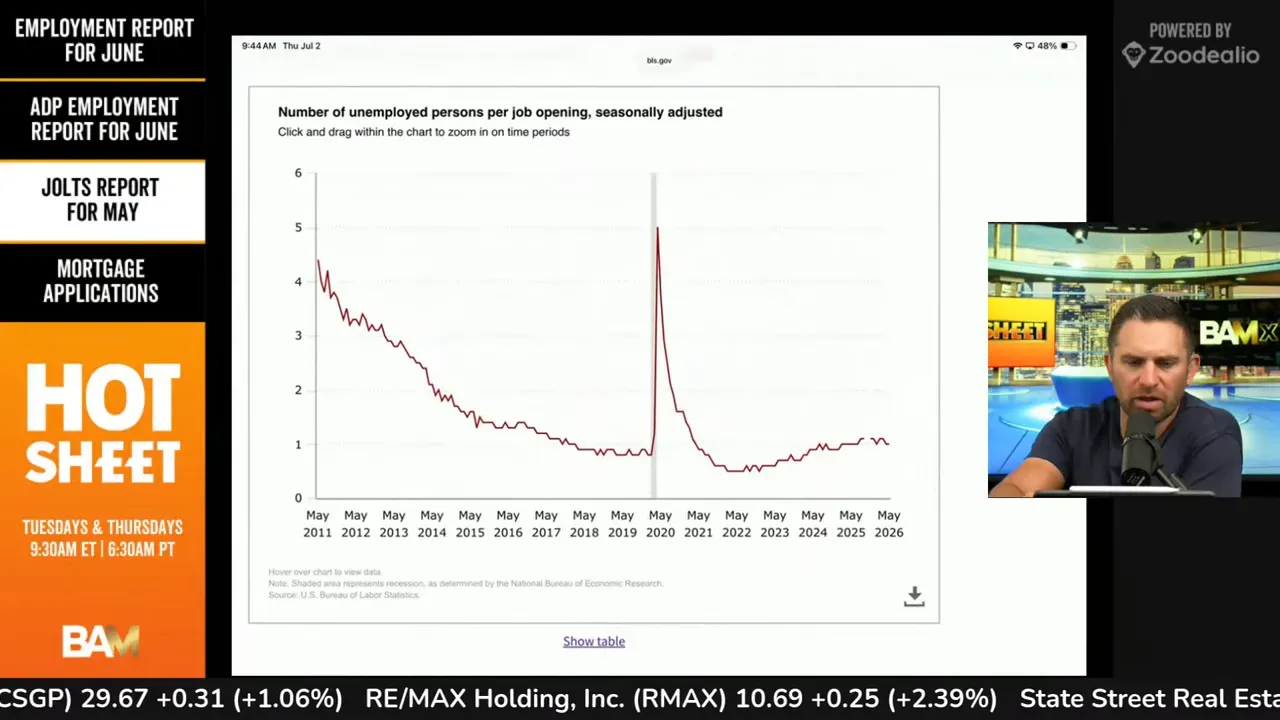

- Job openings were unchanged at 7.6 million in May

- Hires were unchanged at 5.2 million

- Annual pay growth was 4.4%

That mix is not recessionary. It is better described as slower hiring with still-tight labor conditions.

🏦 Why this matters for the Fed

The Federal Reserve works under a dual mandate: maximum employment and stable prices. That means labor data and inflation data are both central to rate decisions.

Right now, the employment side of the equation is not weak enough to create urgency. An unemployment rate of 4.2% is still historically low. Even though June payroll growth missed expectations, the broader labor market does not appear to be under serious stress.

That matters because the Fed is much more likely to cut rates aggressively when unemployment is rising sharply or job losses are broad and persistent. Neither condition showed up here.

At the same time, wage growth of 4.4% can keep pressure on inflation. Rising pay is positive for workers, but from the Fed’s point of view it can also slow the return to lower inflation if it remains sticky.

In plain English: cooler hiring alone is not enough. If prices remain a concern and unemployment stays low, the Fed has little reason to rush into easier policy.

📉 Did the jobs report actually show weakness?

Yes, but only in a limited sense.

The June payroll number of 57,000 was lower than the prior few months and below what many expected. That supports the idea that hiring is cooling. But context matters.

Here is what the data did not show:

- A jump in unemployment

- A collapse in job openings

- A broad drop in hiring across the board

- An obvious labor-market shock

Instead, the reports suggested a gradual slowdown. That is meaningful, but it is not the same as a downturn severe enough to force mortgage rates materially lower in the near term.

One useful way to think about it is this:

- Weak enough to cool the economy a bit

- Not weak enough to change the Fed’s stance by itself

💼 What ADP added to the story

The ADP report showed 98,000 private-sector jobs added in June. That was stronger than the nonfarm payroll headline, though the two reports often differ.

ADP also described hiring as uneven. Some sectors gained, while others lagged. Financial activities, trade, transportation, utilities, and health and education services were among the stronger areas. Leisure and hospitality was called out as softer.

ADP’s commentary also pointed to two themes that matter:

- It is taking longer for people to find work

- Some industries still face labor supply constraints

That combination supports the broader conclusion that the labor market is no longer running hot, but it is not loose either.

For buyers who are also trying to understand financing options in a high-rate environment, this Orlando home buying guide can help clarify down payment strategies and mortgage tradeoffs.

📌 What JOLTS says about labor market tightness

The JOLTS report for May showed 7.6 million job openings, essentially unchanged, with hires steady at 5.2 million.

That is important because it suggests the labor market is still relatively balanced from an employer-demand perspective. A key point in the breakdown was that the market is sitting near a one unemployed person per one job opening relationship.

That is far from a deeply distressed jobs environment.

When job openings stay elevated and hiring does not collapse, the Fed can reasonably argue that the labor market is still functioning well. That makes it harder to justify near-term rate cuts designed to support employment.

🏠 What this means for mortgage rates right now

If you were hoping a softer jobs report would quickly send mortgage rates lower, the current setup is frustrating.

The 10-year Treasury yield was running around 4.475%, and the 30-year fixed mortgage rate was around 6.65%. That kept mortgage pricing near the upper end of this year’s daily readings.

Why did rates stay high even with softer job growth?

- Unemployment is still low

- Wage growth is still firm

- Job openings are still elevated

- The labor market is not showing enough pain to force a policy pivot

Mortgage rates do not move based on one headline alone. They respond to the broader path of inflation, Treasury yields, Fed expectations, and risk sentiment. A single weak payroll print can help, but not if the rest of the labor picture still looks durable.

📈 What mortgage application data is telling us

Mortgage applications rose 0.4% from the prior week, which is basically flat. The more important figure for housing demand was the purchase index.

Purchase applications were:

- Up 1% week over week on a seasonally adjusted basis

- Up 11% unadjusted from the previous week

- Up 3% from the same week a year ago

Those numbers suggest that purchase demand is not dead, even with affordability still stretched.

That aligns with another notable point in the market update: June pending sales showed a surprising increase. In other words, pent-up demand is still showing up when buyers get even modest rate relief or find the right property.

This is one reason the market can feel confusing. Rates remain high, affordability is difficult, yet activity has not vanished. Some buyers have adjusted. Some sellers are still getting traction. And limited inventory can keep deals moving even when financing is expensive.

Selling or buying in Central Florida?

I'm Aleksey Volchek - agent with kardosh Realtly

Schedule an Interview🧠 Why stocks rose on a weaker jobs headline

One interesting market reaction was that stocks moved higher even though the jobs number missed expectations.

That may seem backward, but the logic is fairly straightforward. Equity markets can welcome softer job growth if investors think it lowers future inflation pressure or reduces the odds of further tightening.

So while the labor data was not weak enough to force the Fed’s hand, it may have been soft enough for stock investors to see a slightly friendlier path ahead.

That is a good reminder that stocks, bonds, and mortgage rates do not always respond in the same direction. Housing professionals and buyers should be careful not to assume that a green stock market automatically means lower mortgage costs.

⚠️ Common mistakes when reading jobs reports and rate headlines

There are a few easy ways to misread this kind of update.

Assuming one weak number means rate cuts are coming

It usually takes a broader trend, not a single miss. The Fed will want to see more evidence that labor is weakening or inflation is easing.

Focusing only on payroll growth

Payrolls matter, but so do unemployment, job openings, wages, and hiring trends.

Ignoring wage growth

Pay growth of 4.4% is strong enough to keep inflation concerns alive.

Expecting housing demand to freeze whenever rates rise

Real demand can persist, especially when buyers have delayed moves, inventory is constrained, or households need to relocate regardless of rate conditions.

Thinking unemployment at 4.2% is high

Historically, it is still low. That matters for both Fed policy and overall consumer resilience.

🛠️ What buyers and sellers in Central Florida should do with this information

If you are active in the Central Florida market, the practical lesson is not to wait for a dramatic rate drop that may not arrive on your timeline.

For buyers:

- Run numbers at today’s payment, not at a hoped-for future rate

- Ask whether a later refinance could make sense if rates improve

- Compare neighborhoods carefully for value, insurance cost, and HOA impact

- Review fundamentals before making offers using a checklist like these essential things to check before buying a home

For sellers:

- Do not assume buyers are gone just because rates are high

- Price to current affordability, not to peak-market memories

- Expect buyers to be payment-sensitive and inspection-conscious

- Prepare for a market that can still move, but with less room for overpricing

If you need broader local support, real estate services in Central Florida should include both market strategy and financing context, not just listing access.

🔍 Questions people are asking right now

Is the labor market weakening in 2026?

Yes, hiring appears to be slowing. But based on the June and May data discussed here, it is weakening gradually, not falling apart.

Will the Fed cut rates because job growth missed expectations?

Not based on this data alone. Unemployment remains low, job openings are steady, and wage growth is still relatively strong.

Why are mortgage rates still high if hiring cooled?

Because rates depend on the full inflation and labor picture, not just one payroll number. The market still sees enough economic strength to keep yields elevated.

Are buyers still active despite high rates?

Yes. Purchase applications were slightly higher, and pending sales in June showed better-than-expected movement.

Should buyers wait for lower rates?

That depends on finances, local inventory, and time horizon. Waiting only makes sense if it improves your full position, not just your rate hope. Buyers should also compare current loan structures using tools and education from sources like the Mortgage News Daily rate tracker and the Bureau of Labor Statistics for primary data releases.

✅ Bottom line for the June 28, 2026 market update

Job growth missed expectations, but the broader labor market still looks resilient. Nonfarm payroll growth slowed to 57,000, ADP showed 98,000 private jobs added, unemployment held at 4.2%, job openings stayed at 7.6 million, and wages rose 4.4% year over year.

That is enough cooling to get attention, but not enough weakness to give the Fed a clear reason to ease. As a result, mortgage rates remain elevated, with the 30-year fixed near 6.65% and the 10-year Treasury around 4.475%.

For housing, the message is nuanced. Affordability is still difficult, but demand has not disappeared. Purchase applications and pending sales suggest that motivated buyers are still in the market.

The most accurate summary is this: the labor market is softer, not soft. And until that changes more decisively, mortgage relief may stay limited.

This article was created from the video Job Growth Misses Expectations As Hiring Cools with the help of AI.